Introduction:

Your bank just invested heavily in mobile app optimization. The UX is flawless. Load times are lightning-fast. Customer ratings improved from 3.2 to 4.1 stars in the first month.

Yet engagement metrics haven’t budged.

This paradox reveals a painful truth:

Digital frontends improved, but the backend is still broken

Banks are investing billions in digital transformation and mobile app optimization strategies, yet 62% report that their mobile and online channels fail to deliver expected ROI. The reason isn’t UI/UX. It’s not feature parity. It’s disconnected systems, poor omnichannel architecture, and slow processes that make the customer journey fragmented.

A customer can open an account on mobile in 5 minutes but takes 3 business days to activate it because the backend systems aren’t integrated. A transaction flags as fraud and is blocked immediately, but the investigation takes 18 hours because backend data silos prevent fraud teams from accessing cross-channel context.

This blog explores the real barriers to mobile engagement and how leading banks are fixing customer journey breakdowns.

Mobile App Optimization Strategy: Why Frontend Fixes Don’t Drive Engagement

Modern banking apps are engineering marvels. They feature:

- Real-time push notifications

- Biometric authentication

- One-tap payments

- Personalized product recommendations

Yet despite mobile app optimization efforts, daily active users stagnate. Session duration drops. Feature adoption plateaus.

The reason?

Customers encounter friction the moment they hit backend processes.

Where the Breakdown Happens?

A customer initiates a wire transfer on a mobile (2 seconds). The request routes to a legacy core banking system built in 2008 (5-second latency). That system can’t confirm available funds without querying a separate lending platform (8-second latency). The lending platform requires real-time access to compliance data stored in an isolated data warehouse (12-second latency).

Total journey time: 27 seconds. The customer has already abandoned the transaction.

This isn’t a mobile app problem. This is a systems integration problem masquerading as a user experience problem.

The Investment Trap

Banks responding to poor engagement typically:

- Redesign the mobile interface (costly, 6-month project)

- Add new features (faster, more engagement-focused)

- Improve app performance (technical optimization)

None of this address the core issue: the backend systems still can’t deliver seamless customer experiences across channels.

Backend System Integration: The Real Culprit Behind Low Mobile Engagement

The average bank operates 8–12 core systems: deposits, lending, payments, investments, compliance, risk, operations, and customer data platforms. These systems rarely “talk” to each other. Instead, they operate in silos.

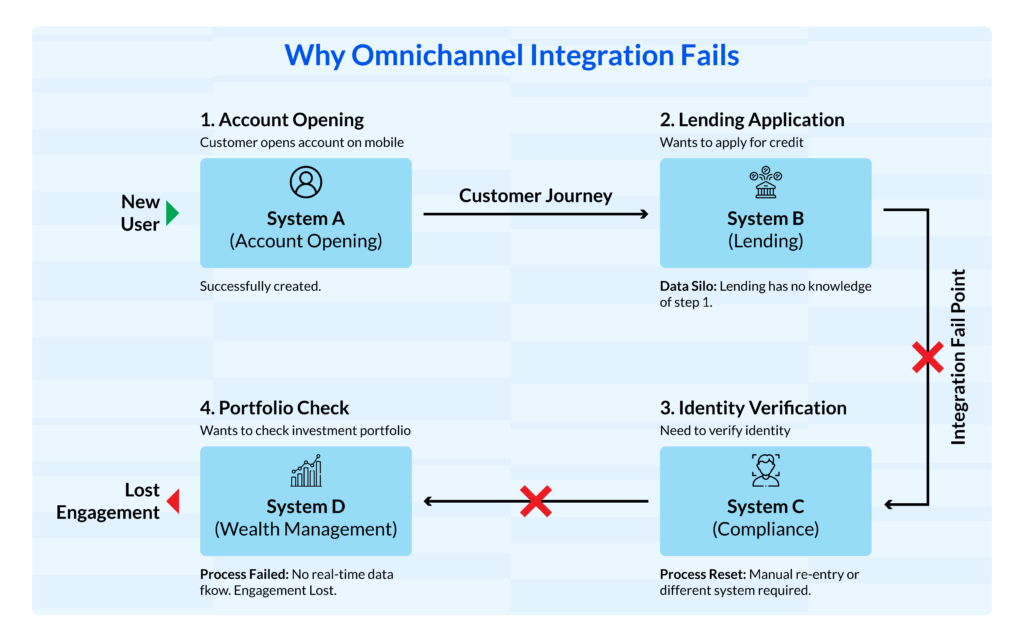

Why Omnichannel Integration Fails

Each system requires separate authentication. Each system has incomplete customer data. Each system requires manual handoffs between channels.

Result: The same customer has 4 different user experiences across the same bank.

The Cost of Disconnection

- Duplicate data entry: Customers repeat information across channels

- Inconsistent product visibility: Loan offers appear on web but not mobile

- Delayed processing: Customer service reps can’t access complete transaction history

- Regulatory exposure: Compliance violations occur because systems don’t sync

- Fraud vulnerability: Account takeover goes undetected because fraud systems don’t access cross-channel behavior

According to Forrester, banks with poor omnichannel integration experience 3x higher customer churn and 40% longer complaint resolution times.

Customer Journey Mapping: How Mobile App Optimization Fails Without Backend Support

Backend fragmentation creates specific friction points where customers abandon the mobile experience.

High-Impact Journey Breakdowns

Onboarding: Customer completes KYC on mobile in 8 minutes. Backend integration delays send account activation email 22 hours later. The customer has moved to a competitor.

Transaction Processing: Fraud detection flags a legitimate purchase (milliseconds). The investigation team doesn’t have cross-channel context (no access to customer’s typical spending patterns). Legitimate transaction blocked.

Customer frustration equals uninstall.

Customer Service: Chat agents on mobile can’t access customer’s wire transfer history because they’re stored in a separate payment system. Agent provides generic response. Customers call branch.

Cost per inquiry: $35 (mobile) → $45 (branch).

Cross-Sell Failure: Customer eligible for credit on mobile doesn’t see offer because lending system and account platform don’t sync. The same customer sees an offer on the web 3 hours later. Opportunity is lost.

These breakdowns compound. First friction point: customer tolerates it. Third friction point: customer switches banks.

Mobile App Performance Optimization: Fixing Backend Integration Issues

Leading financial institutions recognize that mobile engagement requires more than prettier interfaces. They’re fixing backend architecture.

Strategy 1: API-First Architecture

Rather than patching legacy systems, forward-thinking banks are building API layers that sit between customer-facing channels and core systems. This approach:

- Enables real-time data sharing without replacing legacy systems

- Allows mobile, web, and branch to access unified customer data

- Reduces time-to-market for new features

- Minimizes regulatory risk during system modernization

From Systems That Constrain to Platforms That Enable

Book A Application Modernization Call

Strategy 2: Cloud-Native Data Platforms

Legacy data warehouses can’t keep up with omnichannel demands. Cloud platforms enable:

- Real-time data synchronization across systems

- 24/7 availability (no batch processing windows)

- Scalability for millions of simultaneous transactions

- Compliance-ready infrastructure

Banks migrating to cloud-based customer data platforms report 60% faster transaction processing and 45% reduction in manual handoffs.

Prudent’s Cloud Platforms solutions accelerate cloud migration, ensuring your bank’s infrastructure supports true omnichannel experiences.

Mobile App Optimization ROI: Why Backend Modernization Outperforms UI Redesigns

Here’s the financial reality:

The data is clear: Frontend improvements yield diminishing returns. Banks that simultaneously modernize backend systems and redesign frontends achieve 6–8x higher ROI.

Why?

Because users can now actually complete transactions, access consistent data, and experience frictionless journeys across channels.

Digital Banking Challenges: Why Mobile App Optimization Remains Incomplete

Despite growing investment, banks face persistent obstacles in building truly omnichannel experiences:

Technical Challenges

- Legacy System Constraints: 40-year-old core banking systems weren’t designed for real-time data sharing

- Data Fragmentation: Customer data spread across 12+ systems with no single source of truth

- Regulatory Complexity: PSD2, Open Banking, and compliance mandates require careful API design

Organizational Challenges

- Siloed Teams: Mobile teams, backend teams, and compliance teams work independently

- Skills Gap: Hiring engineers who understand both legacy systems and modern architectures is difficult

- Budget Constraints: Board approval for $5M+ infrastructure projects requires clear ROI

Operational Challenges

- 24/7 Availability Requirements: Any system downtime impacts all channels simultaneously

- Security & Fraud Prevention: More integrations create more attack surfaces

- Customer Expectations: “It works on Apple Pay but not your app” erodes trust

These challenges explain why most bank CIOs admit their omnichannel strategy is incomplete.

The Future of Mobile Banking: Beyond Surface-Level App Optimization

The next phase of banking isn’t about mobile apps. It’s about invisible infrastructure.

What’s Changing

From: Digital transformation theater (new app every 2 years) To: Fixing customer journey breakdowns (sustainable backend modernization)

From: Channel-specific experiences (mobile app, web portal, branch) To: Unified customer experiences (same functionality everywhere)

From: Batch processing (overnight settlements) To: Real-time processing (instant account opening, fraud response)

Banks investing in next-generation architecture today will capture market share from competitors stuck in yesterday’s digital transformation cycle.

The competitive advantage isn’t a better mobile app. It’s a backend that enables what the app promises.

How to Optimize Your Mobile App: Fix Backend Integration First

Your mobile app improvements didn’t fail because the design was wrong. They failed because disconnected backend systems can’t deliver the seamless experiences the interface promises.

The path forward requires three things:

- API-First Architecture: Enable real-time data sharing between legacy and modern systems

- Cloud-Native Platforms: Build infrastructure that supports omnichannel at scale

- Organizational Alignment: Break down silos between mobile, backend, and compliance teams

Banks that move from surface-level digital redesigns to fundamental backend modernization will see engagement metrics shift dramatically. Not because the app looks better, but because it actually works better.

Your customers don’t care about your technology stack. They care about whether they can open an account in 5 minutes and activate it in 5 more. Whether fraud investigations take hours instead of days. Whether they get consistent service across mobile, web, and branch.

Fix the backend. Watch engagement rise.

Ready to Fix Your Backend Integration?

Prudent Consulting specializes in helping financial institutions modernize their infrastructure and close customer journey breakdowns.

Schedule a Digital Maturity Assessment