Despite modern data infrastructure, real-time dashboards, and faster pipelines, many banks still struggle with broken loan decisioning. Because faster data movement means little when customer data is fragmented, risk logic is inconsistent, and decision outputs cannot be trusted.

The majority of data and analytics investments fail to deliver measurable business outcomes not because the data is bad, but because the layer between data and decisions was never built.

For US lending institutions, this cost compounds. Every optimization cycle run without addressing the decisioning layer widens the distance between traditional lenders and digitally native competitors.

The result is operational drag at scale: underwriters overriding models, manual reviews increasing, compliance scrutiny intensifying, and expensive modernization programmes delivering little measurable impact on lending performance.

The answer is uncomfortable: you optimized the wrong layer. This piece exposes exactly where loan decisioning process optimization fails, why weak data-driven decision-making is the structural root cause, and what it actually takes to close the gap.

The Failure Pattern Most Lenders Don’t See Until It’s Expensive

Loan decisioning optimization fails at the decision logic layer, not at the data layer. And the failure is nearly invisible from inside the institution experiencing it.

Here is the pattern.

A lender modernizes its data infrastructure. Latency drops. Reporting becomes real-time. Yet approval timelines stay unchanged, exception queues keep growing, and default rates do not improve.

The infrastructure evolved. But the decisioning layer never did.

Speed without decision intelligence is just faster access to the same wrong answers.

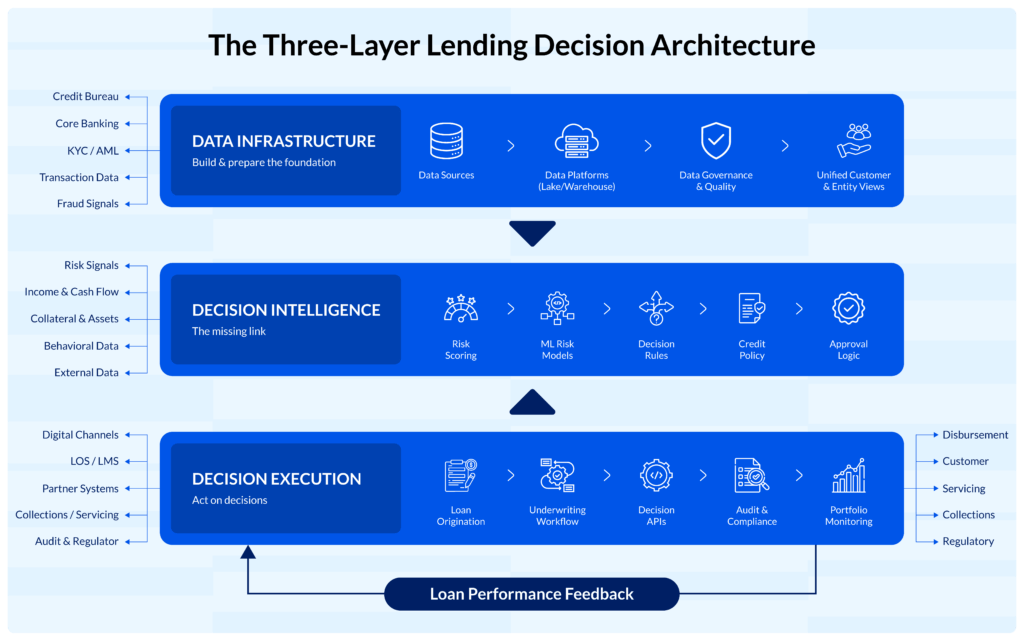

The Three Layers of Loan Decisioning

Most lenders have a detailed technical view of their data layer. Most cannot map the three-layer structure that separates data ingestion from credit decisions.

- Layer 1 — Data Infrastructure: Ingestion, storage, pipelines, quality controls. Where almost all modernization budget lands.

- Layer 2 — Decision Intelligence: Logic, models, and rules that convert data signals into lending actions. Where almost all failures originate.

- Layer 3 — Decisioning Execution: The system that runs, records, and audits decisions at scale with consistency.

Layer 2 is the gap here.

In most lending organizations, it exists as a legacy rule stack built for a different risk environment or it does not exist in any structured form at all. Every optimization sprint that targets Layers 1 and 3 while leaving Layer 2 intact is spending capital to drive faster into a ceiling.

The lenders winning on decisioning aren’t investing more in data. They’re investing in what happens to data once it arrives.

Why Weak Data-Driven Decision-Making Is the Real Bottleneck

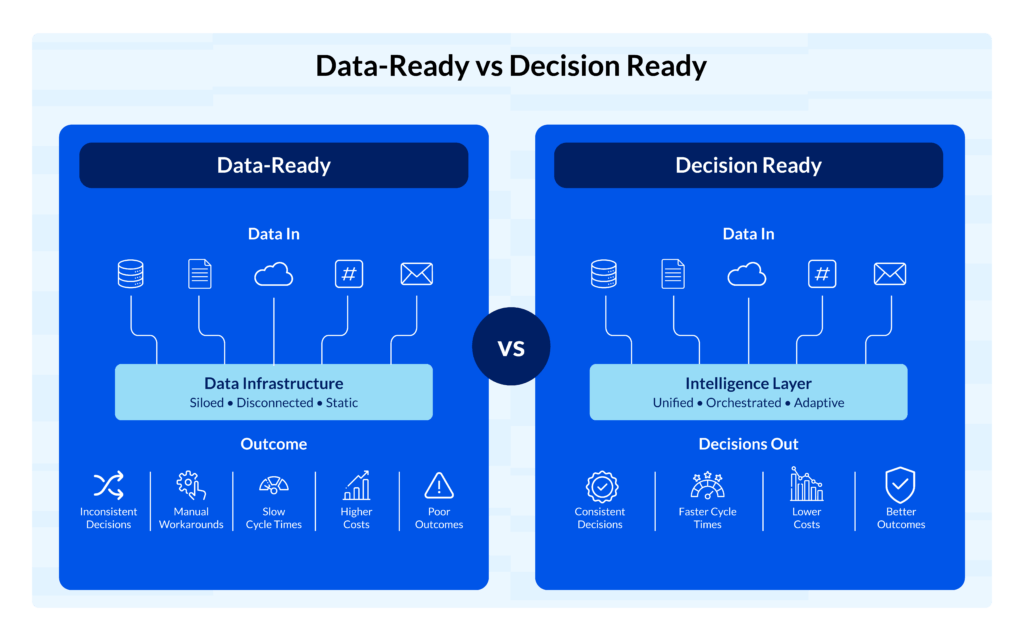

Data-driven decision making in lending is not a dashboard or a reporting capability.

It is the operational ability to convert real-time data signals into lending decisions instantly, consistently, and without manual bottlenecks.

Most lenders have built data accessibility. Very few have built decision accessibility which is the ability to act on risk signals in real time with automation, auditability, and governance built in.

These are not purely infrastructure problems. They are lending data analytics challenges which are the gap between having data and being able to act on it decisively, consistently, and at scale.

Key insight

Financial institutions with mature decision automation outperform peers on both approval speed and default rates simultaneously not as a trade-off, but as a combined outcome. The constraint was never the data. It was the intelligence layer consuming it.

What a Mature Decision-Making Process Looks Like in Lending

A mature data-driven decision-making process in lending has five identifiable characteristics. If your architecture cannot demonstrate all five, there is a gap.

- Dynamic risk models that update continuously from decision outcome data — not static rules reviewed on an annual cycle

- Signal convergence across credit bureau, fraud, and behavioral data in a unified decisioning layer and not three disconnected systems

- Automated exception routing that reserves human review for genuinely complex cases, not as the system default

- Full decision traceability across every approval, decline, and exception linked to a specific signal and logic rule

- Consistent execution across all channels, products, and geographies without process drift or analyst dependency

If your organization cannot describe its decisioning process at this level of operational precision, the investment has improved reporting speed and not decision intelligence.

Modern lending performance depends on AI and machine learning operating directly inside the decision workflow, not outside it in reporting environments.

But before any decision model can operate reliably, the underlying data must be governed. Decision intelligence is only as reliable as the signals behind it. Without governed, audit-ready data, the decision layer simply scales inconsistency instead of eliminating it.

The architecture below illustrates the difference between data infrastructure and true decision intelligence.

The 4 Specific Failure Points in Loan Decisioning Process Optimization

These are structural patterns repeated across lending institutions that modernized data infrastructure while leaving the decision layer unchanged.

Failure Point 1: Optimizing Data Speed Before Decision Logic

Faster pipelines feed unchanged underwriting rules, so decisions remain slow because the logic was built for manual review environments rather than automated decisioning systems.

Speed of input is irrelevant when the decision framework itself is the constraint.

Failure Point 2: Treating Decisioning as a Compliance Function

When compliance becomes the primary owner of decisioning, automation slows, exception queues grow, and governance gradually turns into operational paralysis.

Decisioning must operate at the intersection of risk, data science, and operations and not inside a single functional silo.

Failure Point 3: Siloed Data Without a Unified Decisioning Layer

Credit, fraud, and behavioral signals remain disconnected across systems, resulting in fragmented decisions and inaccurate risk evaluation.

Fragmented data environments inevitably produce fragmented decision outcomes.

Failure Point 4: No Feedback Loop From Decision Outcomes

Decisioning models that do not learn from outcomes eventually plateau because the architecture has no mechanism for continuous improvement or self-correction.

Static decisioning systems cannot evolve into true decision intelligence.

The fourth failure point is the most expensive and the least visible.A decisioning model that cannot learn from outcomes is not true decision intelligence. It is an expensive rule engine in a newer codebase.

After the first optimization cycle, returns begin to flatten not because execution is weak, but because the architecture itself cannot compound improvements.

Institutions that recognize this early optimize the decision layer.The rest spend years modernizing infrastructure while the decisioning ceiling stays the same

The bottleneck in lending decisioning is rarely the data. It’s the layer between the data and the decision and most optimization roadmaps never touch it.

Is your loan decisioning optimization hitting a ceiling?

The gap is almost always in the decision intelligence layer and not the data infrastructure.

What Avoiding These Failures Actually Requires

The lenders closing the decisioning gap are not investing more in data infrastructure, but they are building the decision intelligence layer that turns data into measurable lending outcomes.

This means using AI/ML models to unify credit, behavioral, and alternative data into real-time, explainable lending decisions with built-in compliance traceability.

Before vs. After: The Decision Intelligence Architecture Gap

The performance differential between a static rule-based underwriting framework and a mature ML-powered decisioning layer is not marginal. It is structural and it compounds.

| Dimension | Static Rule-Based Underwriting | ML-Powered Decision Intelligence |

|---|---|---|

| Approval Cycle Time | 3–7 business days | Minutes to hours |

| Decision Consistency | Variable — channel and analyst dependent | Uniform across all products and channels |

| Risk Model Cadence | Annual manual review cycle | Continuous learning from outcome data |

| Exception Volume | High — manual default for edge cases | Surgically routed — throughput protected |

| Decision Explainability | Implicit in rules, hard to audit | Full signal-to-decision trace per record |

| Default Rate Trajectory | Lagging, hard to move without model reset | Predictive and proactively self-correcting |

The Decision Intelligence Stack

A decision intelligence layer is a five-component architecture, each element performing a specific function in converting data signals into lending decisions at scale.

- Unified signal ingestion: Credit, fraud, behavioral, and alternative data converging in one decisioning input layer

- Dynamic ML risk models: Updating from outcome feedback loops, not from annual manual recalibration

- Automated decision engine: Executing consistent, traceable decisions across all products and channels

- Exception intelligence router: Directing genuinely complex cases to human review while protecting throughput

- Audit and explainability layer: Full signal-to-decision traceability for compliance, governance, and model oversight

Loan decisioning process optimization only delivers when the decision layer is as mature as the data layer. That is the architectural truth most optimization programs miss and the one that explains why data-ready institutions are still producing decisions slowly.

Strategic Shift

The most sophisticated lending institutions have stopped asking how to improve their data. They are asking how to make better decisions with the data they already have. That question leads to a different architecture investment and materially different business outcomes.

Diagnose Your Decisioning Gap

Before committing to another infrastructure optimization cycle, run this diagnostic. Five questions. Honest answers. The results will tell you more than a vendor briefing or a consultant engagement will.

| Diagnostic Question | Red Flag If… |

|---|---|

| How long between data availability and a final credit decision? | Answer is measured in days, not hours |

| How many decisioning steps still require manual human review? | More than 30% of decisions touch a human |

| Do your risk models update from outcome data, or on an annual review schedule? | Annual review is your answer |

| Can every loan decision be traced to a specific signal and logic rule? | The answer is “not always” |

| Is decisioning consistent across channels, products, and geographies? | Inconsistency exists and is accepted as normal |

If you answered “we’re not sure” or gave a red-flag response to more than two of these, the gap is in decision making process design and not data infrastructure. Investing further in the pipeline while leaving the decisioning layer intact is not a roadmap. It is a holding pattern.

The diagnostic is designed to produce clarity, not complexity. Every week of ambiguity in the decisioning layer is a week of compounding cost and compounding competitive exposure.

Move from Data Infrastructure to Decision Intelligence

The real failure point in loan decisioning optimization is the decision intelligence layer, where many lenders still rely on static rule engines that cannot scale, learn, or deliver consistent decisions.

Lenders that close this gap approve faster and smarter, are reducing default risk, exception drag and finally realize ROI from their data investments.

Every optimization cycle run without a decision intelligence layer compounds technical and financial debt.

Financial institutions that recognize this architectural truth first build a structural advantage that is difficult to compete against.

At Prudent, we help lending firms move beyond infrastructure modernization by building governed, scalable, and production-ready decision intelligence ecosystems. Our focus is helping banks transform fragmented lending workflows into intelligent, explainable, and outcome-driven decision systems.

Your data is ready. Your decisioning architecture may not be.

Let’s find out with a Decision Intelligence Assessment built for your lending environment.